Getting the keys to your new car is a fantastic feeling! But what about the insurance part? You may have heard about the 3-year third-party insurance mandate for new car buyers in India and felt a bit confused.

What does this rule from the Supreme Court and IRDAI actually mean for you?

This simple guide breaks it all down. We’ll show you what to do, why it’s required, and how to choose the right policy for your shiny new car. You’ll learn to get the protection you need without overpaying.

What is the 3-Year Third-Party Insurance Mandate for New Car Buyers?

The “Why”: The Supreme Court’s 2018 Ruling

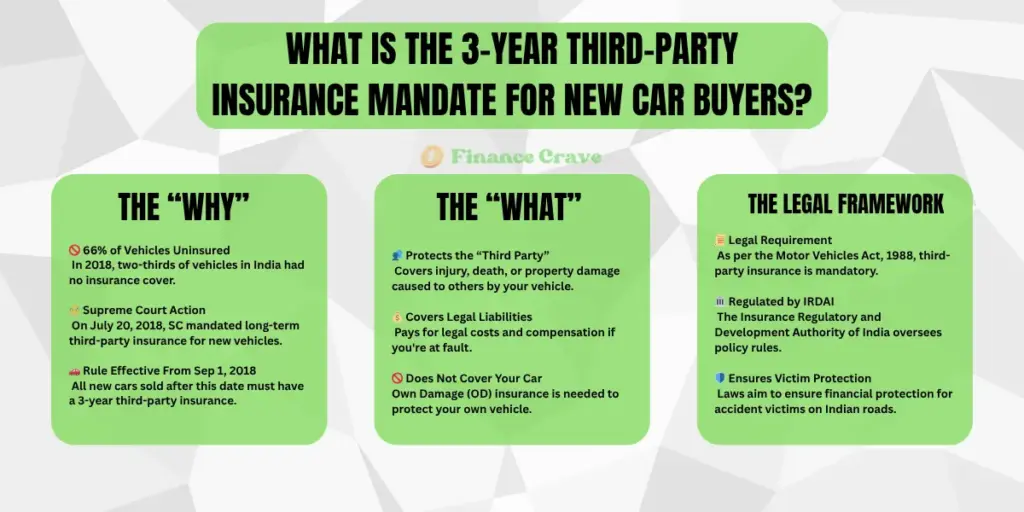

Back in 2018, the Supreme Court of India spotted a big problem. A huge number of vehicles on the road, nearly 66%, didn’t have any insurance cover. This meant that when an uninsured vehicle was in an accident, the victims often got no financial help for their injuries or property damage.

To fix this and protect accident victims, the court made a new rule. On July 20, 2018, it ordered that all new cars sold after September 1, 2018, must come with a three-year third-party insurance policy.

The “What”: Defining Third-Party (TP) Liability Cover

Now, what is “third-party” liability cover? It’s an insurance plan that pays for the legal costs if your car damages someone else’s property or causes injury or death to another person. It’s called third-party because it covers the other person involved, not you or your insurance company.

This policy does not pay for any damage to your own car. For that, you need a different cover called Own Damage (OD).

The Legal Framework: Motor Vehicles Act and IRDAI

This isn’t just a suggestion; it’s the law. The Motor Vehicles Act of 1988 requires every vehicle on Indian roads to have at least this basic third-party insurance. The Insurance Regulatory and Development Authority of India (IRDAI) sets the rules for these policies, making sure they provide the necessary protection for everyone.

Your Insurance Options for a New Car in 2025

When you buy a new car, you have a few ways to get the right insurance cover. Let’s look at what’s available for you today.

Option 1: The Bundled Policy (3-Year TP + 1-Year OD)

This is the most common and practical choice for new car buyers in India. It’s a package deal. You pay for your three-year Third-Party (TP) insurance all at once, which takes care of the legal rule. Along with this, you get a one-year Own Damage (OD) cover.

The OD part protects your own car from damage or theft. After the first year, you just need to renew the OD portion of your policy. This gives you great flexibility, as you can shop around and switch to a different insurance company for your OD cover if you find a better price or service.

Option 2: Standalone 3-Year Third-Party Policy

This is the absolute minimum you need to legally drive your new car out of the showroom. You buy a single policy that covers your third-party liability for three full years. You pay the premium once, and you are set from a legal standpoint.

But remember, this option offers zero protection for your own car. If your car gets stolen or damaged in an accident, a standalone TP policy will not pay for your repairs or loss. You would have to buy a separate Own Damage policy to get that kind of protection.

What Happened to the 3-Year Comprehensive Policy?

You might have heard about a policy that covers both TP and OD for three years together. These were called long-term comprehensive policies. However, the IRDAI stopped insurers from selling these for new cars in August 2020. The main reason was to make new cars more affordable, as the upfront cost of these policies was quite high for many buyers.

While the insurance regulator did propose bringing back these long-term covers in late 2022, the bundled policy (3-year TP + 1-year OD) remains the primary option available to you in 2025.

The Mandatory Add-On: Compulsory Personal Accident (PA) Cover

On top of your vehicle insurance, you must also have a Compulsory Personal Accident (PA) cover. This is a separate but required policy for the owner-driver. It provides a safety net of up to ₹15 lakhs in case of injury or death from a road accident.

Difference between Bundled (3+1) and Standalone TP

Deciding between your insurance options can feel tricky. So, let’s put the two main choices side-by-side to help you see which one fits you best. This quick comparison will show you the key differences in what you pay, what you get, and what works for most new car owners like you. I will use my expertise in insurance content to make this clear and simple.

| Feature | Bundled Policy (3-Year TP + 1-Year OD) | Standalone 3-Year TP Policy |

|---|---|---|

| Upfront Cost | Higher, as it includes the premium for Own Damage (OD) cover for the first year. | Lower, because you only pay the premium for the three-year Third-Party (TP) policy. |

| Coverage | Meets the legal rule and protects your own car from damage or theft for one year. | Only meets the legal rule. It offers no cover for damage to your own car. |

| Flexibility | High. You can renew the one-year OD portion with any insurer you like to find a better price. | High. You have the freedom to buy a separate OD policy from any company at any time. |

| Convenience | Fairly convenient, but you do need to remember to renew the OD policy every year. | Requires you to actively remember to shop for and buy a separate OD policy to protect your car. |

| Best For | Nearly all new car buyers. It gives you a great balance of legal compliance, protection for your car, and choice. | Buyers on an extremely tight budget who understand and accept the risk of driving without any cover for their own car. |

As you can see, the bundled policy is a popular choice because it provides that immediate protection for your own car, which is very reassuring when you’ve just made a big purchase. While the standalone third-party policy is cheaper at first, it leaves your new vehicle completely exposed to the costs of accidental damage or theft, which could be a very big financial loss.

The Financial Impact: Costs, Savings, and the NCB Puzzle

Understanding the cost of your new car’s insurance is a big part of budgeting. Let’s break down what you pay, how you save, and how claim-free driving rewards you. As a writer with deep experience in insurance topics, I’ll make this simple for you.

Upfront Costs & Premiums

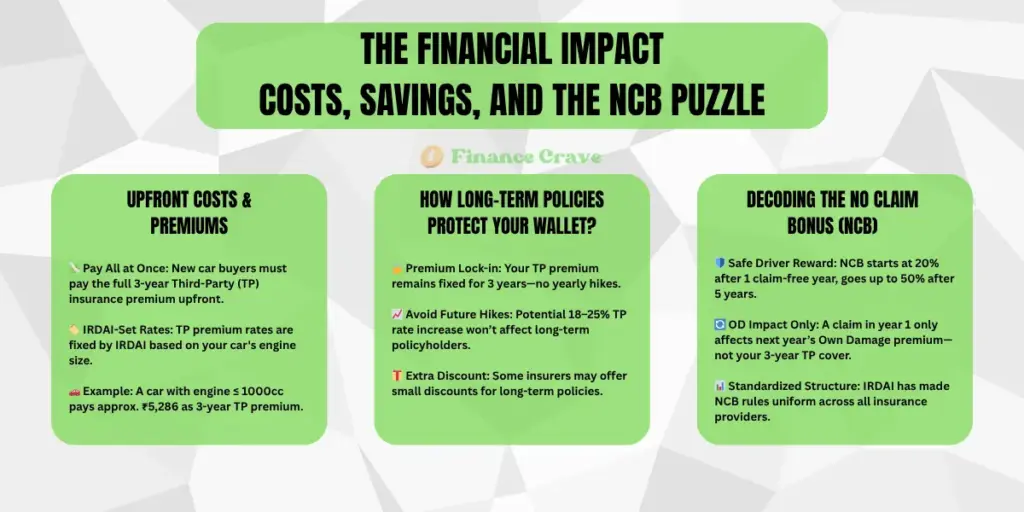

When you get your new car insurance, you pay for the entire three-year Third-Party (TP) policy at once. The government’s insurance authority, IRDAI, sets these rates based on your car’s engine size.

For example, the 3-year TP premium for a car with an engine not exceeding 1000cc is around ₹5,286. If you choose a bundled plan, you will also pay the one-year Own Damage (OD) premium on top of this.

How Long-Term Policies Protect Your Wallet?

Buying a three-year TP policy has a great money-saving benefit. It locks in your premium rate for the full three years. This protects you from the annual price increases that IRDAI often announces.

For instance, reports suggest a potential 18-25% hike in TP premiums could happen soon. By getting a long-term policy, you avoid such increases. Insurers may also offer you a small discount for this long-term commitment.

Decoding the No Claim Bonus (NCB)

The No Claim Bonus (NCB) is a reward your insurer gives you for being a safe driver and not making any claims. It’s a discount on your Own Damage premium when you renew, starting at 20% after one claim-free year and going up to 50% after five years.

With a bundled policy, if you make a claim for your own car’s damage (OD claim) in the first year, you only lose the NCB discount for your OD renewal in the second year. Your three-year TP cover and its cost are not affected at all. IRDAI has made the NCB discount structure the same for all insurance companies, so it’s easy to understand.

A Practical Buyer’s Guide: Making the Smart Choice

Alright, you know about the types of policies. Now, let’s talk about how you can actually pick the best new car insurance without any confusion. I’ll use my expertise to guide you through this.

Can I Buy Insurance Online or Must I Use the Dealer?

You might hear that you have to buy insurance from your car dealer, but that’s not true! You absolutely have the right to choose where you buy your policy. You can look at different plans online, compare prices from various insurance companies, and pick the one that suits you best. Buying online can often save you money and is super convenient too.

Essential Add-Ons to Consider for a New Car

Your basic policy covers a lot, but add-ons give you extra protection. Here are three popular ones for new cars:

- Zero Depreciation: When your car needs a new part after an accident, the insurance company usually pays less for it because the old part was, well, old. This add-on means you get the full cost of the new part without any deduction for wear and tear. It’s really good for new cars.

- Return to Invoice: Imagine your new car gets stolen or is so badly damaged it can’t be repaired. With this add-on, the insurance company will pay you the car’s original showroom price (the amount on your bill), not just its current lower value.

- Engine Protection: This is a lifesaver if you live in an area where it floods or if there’s damage to your engine from water or oil leakage. Regular policies often don’t cover this, so engine protection is a smart pick for many.

Checklist: Questions to Ask Your Insurer/Dealer

Before you say “yes” to any policy, ask a few smart questions. This helps you understand exactly what you are getting. Here’s a quick list:

“What is the exact No Claim Bonus (NCB) I will get if I don’t make a claim?”

“If I sell my car in a year or two, how does the insurance get transferred to the new owner?”

“What is the standard compulsory deductible for my car model?” (This is a small amount you pay from your pocket during a claim, like ₹1000 for cars under 1500cc).

Potential Insurance Changes in 2025

As an insurance writer, I see the landscape is always evolving. For 2025, you should be aware of a few upcoming changes.

The government is reviewing a proposal to increase third-party premiums by an average of 18%, with some vehicle types possibly facing a 20-25% hike. This is because rates haven’t changed in four years, while claim costs have gone up.

CNBC-TV18 Exclusive | @MORTHIndia is considering hiking Motor 3rd Party #premium for FY26. Sources say that #RoadMinistry has received recommendations from #IRDAI seeking an average 18% increase in premium. @YashJain88 pic.twitter.com/8dzp1XFK9z

— CNBC-TV18 (@CNBCTV18News) June 6, 2025

At the same time, the insurance regulator IRDAI is introducing rules for a faster, more transparent claims process, which is great news for policyholders. This includes a mandatory Customer Information Sheet to help you understand your policy better, making the whole system fairer.

Ending Note

The 3-year third-party insurance mandate is designed to protect everyone on the road. For most people buying a new car, the bundled policy (3-Year TP + 1-Year OD) provides the best mix of legal compliance, financial protection, and flexibility.

Always compare quotes, understand your NCB terms, and choose the policy that truly fits your needs.

Frequently Asked Questions

Is it mandatory to buy 3-year insurance for a new car?

Yes. The law in India requires every new car to have a third-party (TP) liability insurance policy that is valid for three years from the date of purchase.

What does a 3-year third-party policy cover?

This policy covers your legal and financial responsibility if your car causes injury, death, or property damage to another person (a third party). It does not cover any damage to your own car.

What are my main insurance choices for a new car?

You can either buy a standalone 3-year third-party policy or a bundled policy. The bundled option includes a 3-year third-party cover along with a 1-year own-damage (OD) cover for your car.

Can I sell my car if it has a long-term policy?

Yes. If you sell your car, the remaining period of your 3-year third-party insurance can be transferred to the new owner. The new owner must apply for the transfer within 14 days of the purchase.

Do I also need a Personal Accident cover?

Yes. Along with the car’s insurance, it is also compulsory for the owner-driver to have a Personal Accident (PA) cover for at least one year.